The Coronavirus Economic Response Package (Payments and Benefits) Amendment Rules (No. 8) 2020 legislative instrument was registered last Tuesday, setting out the decline in turnover test for the extension of JobKeeper to 28 March 2021 and the new two-tiered payment rates.

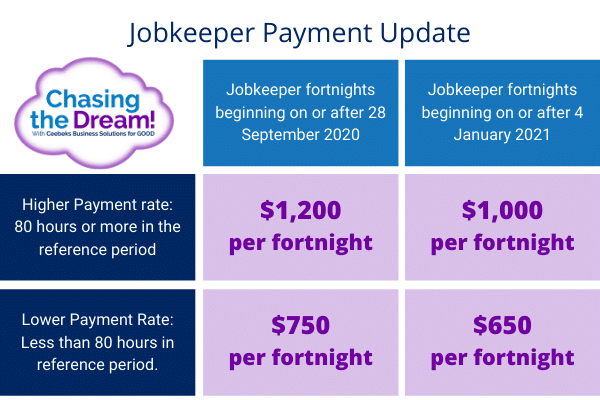

For the first extension period running from 28 September 2020 to 3 January 2021, employees who worked for 80 hours or more in the 28 day period before either 1 March 2020 or 1 July 2020 will receive $1,200 per fortnight, while all other employees will receive $750.

For the second period running from 4 January 2021 to 28 March 2021, the rate will drop to $1,000 per fortnight and $650 per fortnight, respectively.

Actual decline in turnover test

Depending on whether an entity was an ACNC-registered charity; a business with a turnover of $1 billion or less, or a business with a turnover of over $1 billion, they will be required to demonstrate a decline of either 15 per cent, 30 per cent, or 50 per cent, relative to its comparable quarter in 2019.

To qualify for the first extension period, entities will need to satisfy the new actual decline in turnover test for the quarter ending 30 September.

To qualify for the second extension period between 4 January 2021 and 28 March 2021, the actual decline in turnover test will need to be applied for the quarter ending 31 December 2020.

The rules stipulate that entities are allowed to qualify for JobKeeper for each extension period if they satisfy the actual decline in turnover test for that quarter, even if they did not previously qualify.

“This new feature of the JobKeeper system recognises that eligibility for later JobKeeper periods needs to take into account the most recent impacts on the turnover of affected businesses to ensure support is targeted to those businesses still significantly impacted by COVID-19,” said the rules.

Determining higher or lower rate

The reference period for employees is the 28 days ending at the end of the pay cycle that finished immediately before 1 March 2020 or 1 July 2020.

The hours include actual hours worked, and any hours for which the employee received paid leave, including annual, long service, sick, carers and other forms of paid leave, or paid absence for public holidays.

For eligible business participants, the test to determine which rate to apply will instead be based on the assessment of the hours that the business participant was actively operating the business or undertaking specific tasks in business development and planning, regulatory compliance or similar activities in an applicable reference period.

The reference period for business participants will be February 2020.

The rules note that entities who fail to notify the Commissioner of Taxation of the relevant rate for an employee will fail to qualify for the JobKeeper payments until a valid notification is made.

Entities will also be required to notify their employees whether they qualify for the higher or lower rate within seven days of notifying the Commissioner.

The Commissioner will be allowed to specify an alternative decline in turnover test, and an alternative reference period for working out if the higher or lower JobKeeper rate applies in respect of eligible employees, business participants, and religious practitioners.

Give us a call if you would like to talk more about JobKeeper.

{kind=link}